(Almost Free Traveling is part of an affiliate sales network and receives compensation for sending traffic to partner sites, such as Milevalue.com. This compensation may impact how and where links appear on this site. This site does not include all financial companies or all available financial offers)

If you’re just getting started using credit card welcome bonuses for travel, welcome! There’s undoubtedly lucrative redemptions enabling almost-free-travel in your future.

There are also potential pitfalls. That’s what today’s post is for: preparing you for possible missteps by setting you up for success!

With that said, here are ten mistakes to avoid when you’re starting out on your journey.

1. Not Having a Plan

The very first thing I ask someone during a credit card consult is “where do you want to go and when?” Begin with then end in mind! Do you have a dream Disney vacation you’ve been longing to take but can’t afford (probably, if you’re reading my blog!)? Do you want to go to Disney and then Hawaii and then Europe after that? Make a plan and then strategize how to get the best value out of the points & miles you earn, which we will touch on later in the transferring points section.

2. Waiting too Long to Start

One you have a plan, don’t delay! Analysis paralysis have you unsure where to start? Seasoned credit card points and miles travelers agree: we wish we had started award travel earlier than we did! Don’t get left behind: if you’re not sure where to start, learn from our mistakes. Read this post that describes exactly which cards we would open for Disney trips if we could have a do-over:

3. Forgetting About Chase’s 5/24 Rule

If you’ve looked into points & miles, you’ve probably heard the numbers 5/24 thrown around. 5/24 pertains to Chase bank and stands for five cards in 24 months. Chase offers many great cards, generous referral bonuses, and the ability to reopen cards and earn bonuses again. Here’s the catch: they will also cut you off from opening cards as soon as you’ve opened any five personal cards from any bank within a rolling 24-month period. For that reason, you should prioritize Chase cards, open business cards, alternate with a friend or family member if possible (more on that next) and always keep track of your 5/24.

4. Not Opening Business Cards

Did you know that you can open business credit cards based on any side income, no matter how small? Even if you don’t have an LLC or tax ID number (I don’t) you can probably open a business card. And the best part of all is that business cards don’t count against your 5/24 (unless it’s a TD Bank, Discover or Capital One Business card).

While Chase business cards don’t count against your 5/24, keep in mind that you have to fall below 5/24 to open a Chase business card. Chase offers some of the best business cards around, including this one:

Open the Chase Ink Business Cash Credit Card and earn $900 bonus cash back after you spend $6,000 on purchases in the first 3 months from account opening. If you want to turn that cash back into 90K Ultimate Rewards you can transfer to airlines and hotels for valuable redemptions, make sure you have a Chase Sapphire Preferred, Reserve or Chase Ink Business Preferred. Those three cards allow points transfers, which we will cover next.

5. Cashing out Points and not Transferring Them

I’ll be very upfront and say that I’ve used and cashed out a lot of points 1:1. There’s nothing inherently wrong with that, UNLESS you’re missing out on travel opportunities you could have unlocked by transferring your points instead of using them 1:1.

For instance: I tell people how to buy Disney tickets using their points & miles, because for some people, their ultimate goal is a free Disney trip. They don’t care about Hawaii or Europe or the Maldives: they want ttheir Disney and they want it to be free. But just know that you’re almost always going to get 1:1 value out of your points if you’re using them for Disney tickets (the exception is using BILT rewards to purchase Disney tickets through their portal, where rewards are worth 1.25. You can even purchase Disneyland Paris tickets with BILT!).

Popular transfers pertaining to Disney include transferring Capital One Miles or Citi ThankYou points to an airline for an international flight to Disneyland Paris–or doubling your Citi ThankYou points by transferring them to Choice hotels 1:2 and booking overseas lodging.

Stateside, transfer Ultimate Rewards to Southwest Airlines to book flights to Disneyland or Walt Disney World–or transfer to Hyatt to book lodging near Disneyland or Walt Disney World:

6. Falling Into the Authorized User Trap

It always seems like a good idea at the time to add your spouse onto your new card as an authorized user–it does make it easier to spend when you both have a copy. But when you’re both actively opening credit cards and working together to amass points & miles, every AU spot counts against your 5/24.

Our authorized user workaround is adding our brand new card to every digital wallet in our household; that way, both spouses and our teenagers can all spend on the new card.

The only card I’m an authorized user on is my spouse’s premium Capital One card, so that we can both use the complimentary Priority Pass feature independently of one another:

A premium card with a $395 annual fee, open a Capital One Venture X Rewards Credit Card and earn 75,000 bonus miles once you spend $4,000 on purchases within the first 3 months from account opening.

7. Being Scared off by Annual Fees

It’s good to be AWARE of annual fees, and to make thoughtful decisions as to whether they are worth paying. We have several airline and hotel cards we keep open because we feel the benefits outweigh the annual fee, and we also keep our Capitol One Venture X premium travel card open for the following reasons.

You pay $395/year for the Venture X, but also receive up to $300 back as statement credits for bookings through Capital One Travel, where you’ll get the best prices on thousands of options. Get 10,000 bonus miles (equal to $100 towards travel) every year, starting on your first anniversary. Receive up to a $100 credit on Global Entry or TSA PreCheck®. Earn 10X Miles on hotels & rental cars booked through Capital One Travel, 5X Miles on flights booked through Capital One Travel, and 2X Miles on all other purchases, every day.

Protect your cell phone every time you pay your bill with your Venture X card. If it’s stolen or damaged, you’ll get reimbursed up to $800 (certain terms, conditions and exclusions apply). Add cardholders to your account for no fee—they can enjoy benefits and you will earn rewards on every dollar they spend. Refer your friends and family to apply for a Venture X card and earn up to 100,000 bonus miles when they’re approved (terms apply). Sign up for complimentary Hertz President’s Circle® status, skip the counter and choose from the widest selection of cars—and enjoy guaranteed upgrades with Venture X. Recharge with all-inclusive amenities like fresh local food options, high-speed WiFi and cozy relaxation rooms with unlimited free Capital One Lounge visits for Venture X cardholders. Bring 2 free guests per visit, $45 per additional guest.

We recently opened the Venture X, completed our minimum spend, and then purchased $572 worth of Disney tickets on the card through Undercover Tourist. Once the charge posted, we used 57,200 miles to erase the ticket charge! This was a good use of points for us because we wanted our tickets to be free, and we didn’t have a lucrative transfer we needed for a future vacation.

The Venture X card is our favorite card, but we have also had buyers remorse opening certain cards and regretting it later.

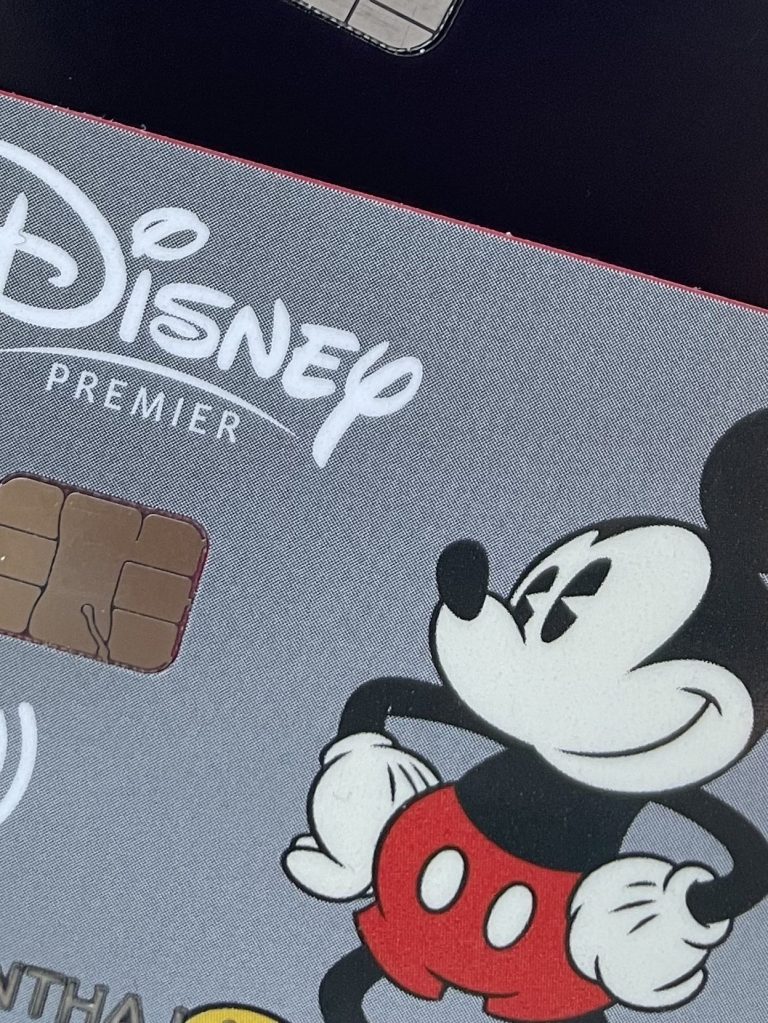

8. Opening Lame Cards

This category is subjective, but there are a few cards that people generally agree should almost never be opened. And–*gulp*–I once opened the worst offender: the Chase Disney card.

The truth is, a couple years ago I got suckered into this credit card because Mickey Mouse is on the front. Reasons I regret this decision: it doesn’t offer a competitive sign up bonus, and the ongoing perks aren’t great either. And when you’re trying to stay under 5/24, it just doesn’t deserve a spot in your card count.

Additionally, if what you really want is a Disney character or castle card, simply open a Chase checking account and request a Disney debit card (read more in this blog post):

9. Opening the Wrong Card First

Make sure the first credit card you ever open is a card you won’t mind leaving open forever. You probably already have at least one credit card in your wallet–that’s fine, just leave it there. But if you don’t, and you need a recommendation, the following card is one you might have in your wallet forever:

10. Missing Elevated Bonuses

There are always certain credit cards that have a higher-than-usual welcome bonus–we refer to those as elevated bonuses. Trying to work those into your strategy without compromising your 5/24 is part of the game! Here’s a few cards with elevated bonuses that are both worth considering for different reasons:

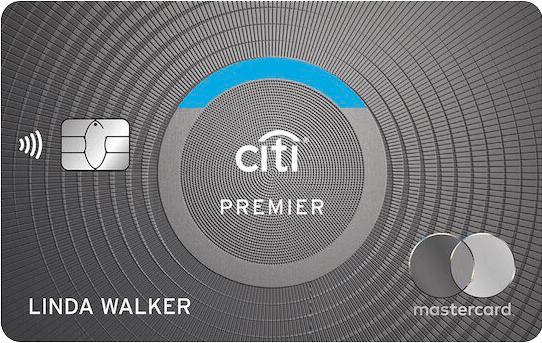

Citi Premier® Card

Earn 80,000 bonus ThankYou® Points after you spend $4,000 in purchases within the first 3 months of account opening, for a $95 annual fee.

PROS: That’s at least $800 worth of travel, and more if you transfer the points to Choice Hotels 1:2 or to an airline for an overseas flight. We combined two Citi Premier bonuses to purchase three-day Disneyland tickets for our family of five in 2019!

CONS: This will take a spot in you 5/24, so make sure it’s worth it. Also, it doesn’t have a personal referral link, so you can’t earn referral bonuses from family and friends.

Capital One® Venture® Rewards Credit Card

Earn 75,000 miles once you spend $4,000 on purchases within 3 months from account opening, for a $95 annual fee.

PROS: That’s at least $750 worth of Disney tickets, or more if you transfer to an airline for an overseas flight to Disneyland Paris. This card will also get you into the Dallas Forth Worth Capital One Lounge twice annually!

CONS: This will take a spot in your 5/24, so make sure it’s worth it. You CAN get personal referral bonuses, but ONLY if the person you are referring has NEVER had a Capital One card before.

Takeaways

All right, no more excuses! You know which mistakes we’ve made and which cards we recommend in what order. Now is the time to start earning and burning points that will save you tons of cash on your next Disney trip and beyond. No matter where you journey takes you, have a magical time!

Learn more about how we travel for almost free on Instagram @almostfreetraveling and join the conversation on facebook.com/almostfreetraveling

Opinions expressed here are author’s alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post. The content on this page is accurate as of the posting date; however, some of our partner offers may have expired.

Leave a comment